For NRIs tax filing in India can become sophisticated, particularly when determining the right return form. Selection of the incorrect return form can cause warning letters, delay in processing and adherence problems. For AY 2026-27, careful evaluation of the various sources of income is important for NRIs before selecting between ITR-2 and ITR-3. Learning the distinction between these forms plays an important role in precise income tax return filing and adhering with the Indian tax laws. This guide talks about the eligibility requirement, major differences and the factors that can help the NRIs select the appropriate return form.

Understanding ITR Forms for NRIs

The Income Tax Department offers various types of return forms to the people depending on the income they have earned throughout the year from various sources.

The most popularly used forms for NRIs are:

- ITR-2

- ITR-3

The selection relies entirely on whether the NRI earns income from business or profession in India.

Before selecting an income tax return form, taxpayers should review all income streams, including salary, house property, capital gains, investments and business earnings.

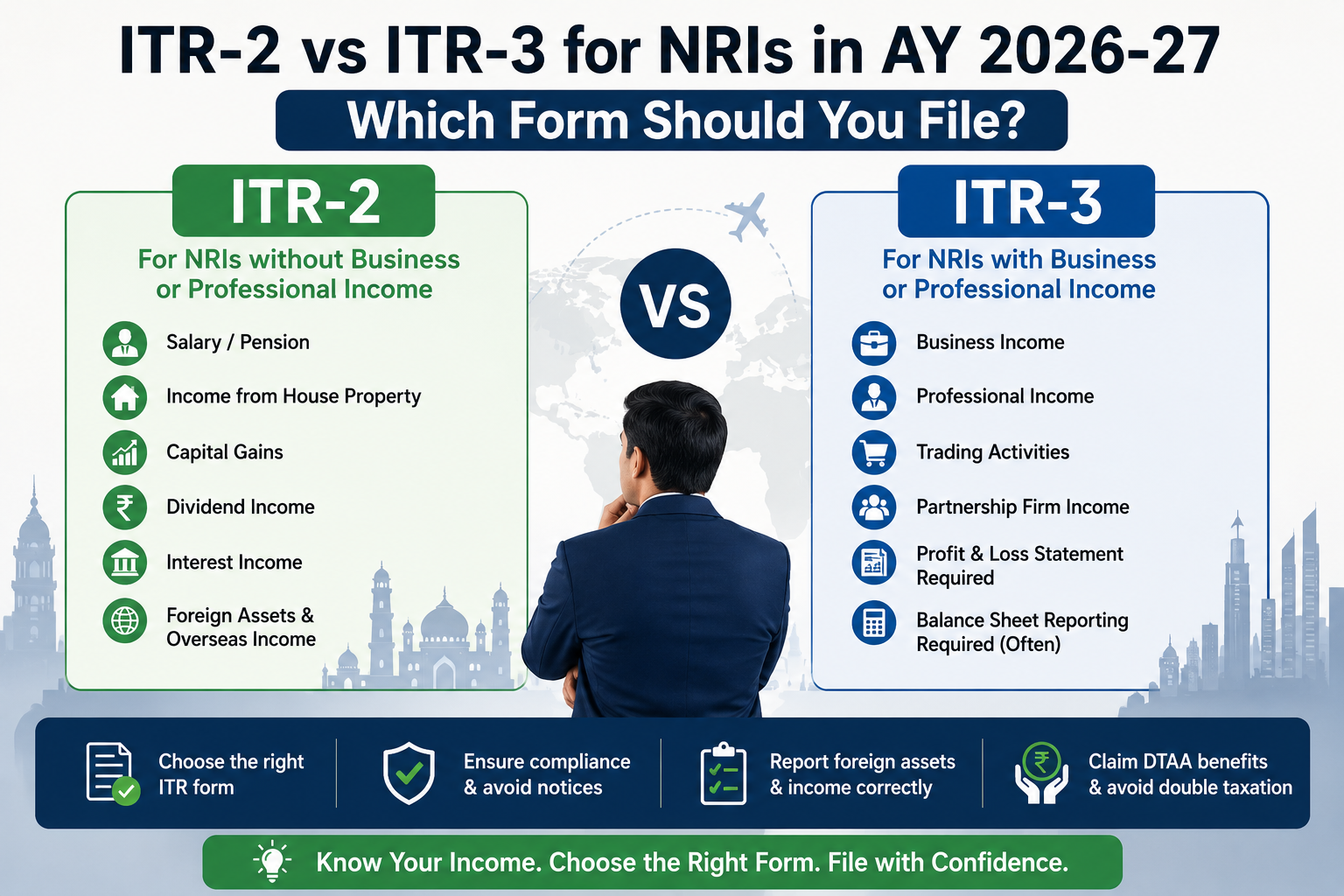

What is ITR-2?

ITR-2 is for individuals and Hindu Undivided Families (HUFs) whose source of income is neither from business nor profession.

An NRI can file ITR-2 when he/she gets income from:

- Salary or pension

- House property

- Capital gains from shares, mutual funds or property

- Dividend income

- Interest income from bank accounts and deposits

- Agricultural income exceeding prescribed limits

- Foreign assets and overseas income disclosures

NRIs with salaries, rental income or investments in India may typically find ITR-2 as an appropriate option.

What is ITR-3?

For individuals or HUFs whose primary income is derived from business or profession, filing of ITR-3 is suitable.

ITR-3 must be filed when an NRI have:

- Proprietorship business income

- Professional income from consultation, freelancing or specialized services

- Income from trading activities

- Partnership firm income where applicable

- Business-related capital accounts and financial statements

For NRIs running businesses or providing expert services in India, ITR-3 becomes required.

ITR-2 vs ITR-3 for NRIs: Detailed Comparison

| Particulars | ITR-2 | ITR-3 |

| Suitable For | NRIs without business income | NRIs with business or professional income |

| Salary Income | Allowed | Allowed |

| House Property Income | Allowed | Allowed |

| Capital Gains | Allowed | Allowed |

| Dividend Income | Allowed | Allowed |

| Interest Income | Allowed | Allowed |

| Business Income | Not Allowed | Allowed |

| Professional Income | Not Allowed | Allowed |

| Maintenance of Books | Not Required | May Be Required |

| Profit & Loss Statement | Not Applicable | Required |

| Balance Sheet Reporting | Not Required | Required in many cases |

| Complexity Level | Comparatively Simple | More Detailed and Complex |

| Tax Audit Applicability | Generally Not Applicable | May Apply Depending on Turnover |

This comparison helps taxpayers identify the correct income tax return itr form based on their income profile.

When Should an NRI File ITR-2?

An NRI should consider ITR-2 if:

- They earn a salary from an overseas employer

- They own residential or commercial property in India

- They receive rental income from Indian property

- They earn capital gains from investments

- They have interest income from NRE, NRO, or fixed deposit accounts

- They need to report foreign assets and overseas earnings

For most of the salaried and investment-oriented NRIs, ITR-2 continues to be the suggested income tax return choice.

When Should an NRI File ITR-3?

ITR-3 should be selected when:

- The taxpayer runs a business in India

- They provide consulting or professional services

- They earn commission-based income

- They operate a sole proprietorship

- They are involved in trading or commercial activities generating business income

Even if salary or capital gains exist alongside business income, ITR-3 must generally be used.

Foreign Income Reporting Requirements for NRIs

One of the most important aspects of NRI taxation is reporting overseas income and assets wherever applicable.

Key disclosure requirements may include:

- Foreign bank accounts

- Foreign investments

- Overseas property ownership

- Foreign stocks and securities

- Income earned outside India

Proper reporting of foreign income tax in India obligations helps prevent penalties and guarantees adherence with international tax openness regulations.

NRIs should also evaluate Double Taxation Avoidance Agreement (DTAA) rules to prevent paying tax twice on the same income.

Common Mistakes NRIs Make While Selecting Return Forms

Many NRIs face tax notices because of incorrect return selection.

Common mistakes include:

- Filing ITR-2 despite having business income

- Ignoring professional consultancy income

- Incorrect disclosure of foreign assets

- Missing capital gain reporting

- Failing to claim DTAA benefits properly

- Selecting forms based entirely on last-year filings

Reviewing income sources yearly is important because eligibility might change from one year to another.

Documents Required Before Filing

To ensure smooth filing, NRIs should keep the following documents ready:

- PAN card

- Aadhaar details (if applicable)

- Passport details

- Bank account information

- Form 16 (if available)

- Rental income records

- Capital gain statements

- Foreign asset details

- Investment statements

- Tax payment challans

- Foreign tax credit documents

Maintaining organized records reduces errors and speeds up return processing.

Checking Return Processing Status

After submission, taxpayers should regularly monitor their income tax return status to ensure successful processing.

The status may indicate:

- Return filed

- Return verified

- Under processing

- Processed successfully

- Refund issued

- Defective return notice

Prompt action on any notices can help prevent unnecessary delays and complications.

Why Professional Guidance Matters for NRIs

NRI taxation involves various complex areas, including housing status determination, DTAA advantages, foreign asset disclosures, foreign tax credits and reporting needs.

Seeking expert assistance can help:

- Select the correct ITR form

- Reduce compliance risks

- Ensure precise disclosures

- Prevent penalties and notices

- Maximize eligible deductions and advantages

For people looking for professional assistance, a qualified nri income tax consultant in Noida can provide personalized advice according to their distinct income structure and international tax regulations.

Conclusion

Selection between ITR-2 and ITR-3 for AY 2026-27 relies heavily on whether an NRIs source of income is business or professional working. ITR-2 is appropriate for salary earners, investors and property owners whereas ITR-3 is mandatory for those involved in business or professional activities. Knowing the nature of income, reporting foreign assets correctly and adhering with disclosure needs are crucial for precise tax filing. AVS & Associates helps NRIs go through these complexities with expert advice, ensuring seamless adherence, right return choice and stress-free tax filing in India.